August 2023: proposed rules

On Aug. 25, 2023, the US Treasury and the IRS launched proposed rules that will require firms engaged in digital asset-related companies to file info returns and furnish payee statements for digital asset inclinations.

The proposed rules present clarification on a number of essential points, together with which digital belongings are topic to reporting, who qualifies as a dealer, how you can calculate foundation in a digital asset and the remedy of digital belongings as a separate class distinct from securities and commodities.

“A key a part of this effort matches in with the bigger IRS compliance concentrate on rich taxpayers. We’d like to ensure digital belongings should not used to cover taxable earnings, and the proposed rules are designed to offer a clearer line of sight into actions by high-income folks in addition to others utilizing them,” stated IRS Commissioner Danny Werfel.

The rules outline “digital asset intermediary” broadly, encompassing entities like buying and selling platforms, pockets suppliers and fee processors. Beneath these proposed rules, brokers could be mandated to report on digital asset gross sales, with an expanded definition of “digital asset.”

These rules are slated to take impact for transactions occurring on or after Jan. 1, 2025, with some reporting points having later efficient dates. It is very important be aware that these rules are nonetheless within the proposal stage and will endure additional revisions.

Definition of digital belongings and brokers

The proposed US Treasury and IRS rules develop the definition of reportable digital belongings to incorporate stablecoins, NFTs and tokenized shares, excluding digital belongings restricted to closed techniques like online game tokens.

A digital asset is a illustration of worth recorded on a safe, distributed ledger. Frequent sorts embody:

- Convertible digital forex and cryptocurrency (e.g., Bitcoin, Ethereum).

- Stablecoins, that are cryptocurrencies pegged to a secure asset like a fiat forex (e.g., USD Coin, Tether).

- Non-fungible tokens (NFTs), distinctive tokens representing possession of digital belongings like artwork or collectibles.

- These digital belongings serve numerous functions inside blockchain and digital finance techniques.

The definition of a “dealer” is broadened to cowl entities offering “facilitative companies” for digital asset gross sales, requiring detailed transaction reporting together with buyer info and sale specifics.

Moreover, the Infrastructure Funding & Jobs Act broadened the definition of “dealer” to incorporate these facilitating digital asset transfers for others. This is applicable to any digital illustration of worth recorded on a distributed ledger.

US tax consultants have been vocal on the dearth of readability in present tax regulation. As an illustration, the proposed regulation § 1.6045–1(a)(21)(iii)(A) defines a facilitative service as any service that instantly or not directly permits a sale of digital belongings. It excludes individuals solely engaged in offering distributed ledger validation companies, like proof of labor or proof of stake, with out providing different features or companies.

Based on a Bloomberg Legislation report, attributable to an absence of readability, many proof-of-stake stakers and staking companies are taking a conservative method. They report the worth of reward tokens as earnings in the mean time they’re created, somewhat than after they truly obtain earnings by promoting their reward tokens.

Monitoring crypto earnings by way of software varieties

The IRS is now monitoring cryptocurrency earnings by asking taxpayers on Kind 1040 about their crypto actions. The shape particularly inquires whether or not people engaged in receiving, promoting, sending, exchanging, or buying digital forex. Offering false info can result in penalties, as tax returns are legally binding statements.

On Jan. 22, 2024, the IRS reminded taxpayers that they should reply a digital asset query and report any associated earnings when submitting their 2023 federal earnings tax returns, just like what was required for the 2022 tax returns.

The query seems on the high of varieties:

- 1040, Particular person Earnings Tax Return;

- 1040-SR, U.S. Tax Return for Seniors;

- 1040-NR, U.S. Nonresident Alien Earnings Tax Return.

- 1041, U.S. Earnings Tax Return for Estates and Trusts;

- 1065, U.S. Return of Partnership Earnings;

- 1120, U.S. Company Earnings Tax Return;

- 1120-S, U.S. Earnings Tax Return for an S Company.

The digital belongings query asks taxpayers whether or not, at any time throughout 2023, they acquired digital belongings as a reward, award, or fee for property or companies, or in the event that they offered, exchanged, or in any other case disposed of a digital asset or a monetary curiosity in a digital asset.

The query might fluctuate barely relying on the kind of taxpayer (particular person, company, partnership, or property/belief). Along with checking the field, taxpayers should report all earnings associated to digital asset transactions.

April 2024: 1099-DA draft type

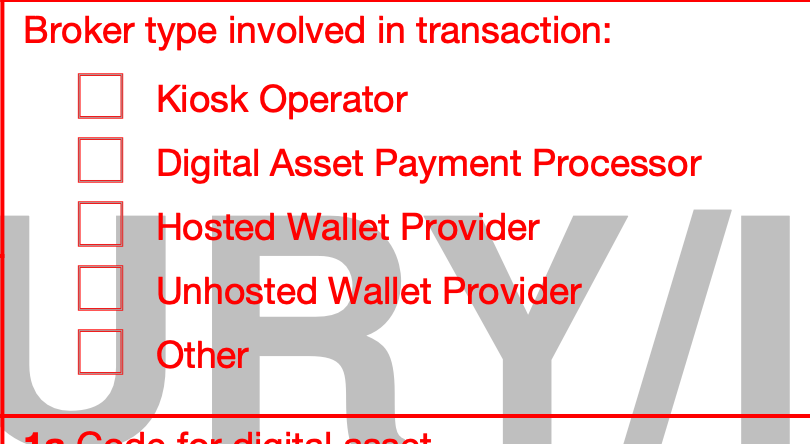

On April 18, 2024, the IRS unveiled a draft of Kind 1099-DA aimed toward calculating taxable positive factors or losses from brokered digital asset transactions. This type contains token codes and fields for pockets addresses, important for reporting to each taxpayers and the IRS.

Kind 1099-DA contains particular person token codes, areas for pockets addresses and particulars on how you can find transactions on the blockchain. Brokers are required to report digital asset inclinations on this way to each taxpayers and the IRS, probably resulting in acknowledged positive factors for taxpayers.

Nevertheless, the cryptocurrency trade stays unsure about how the IRS will establish brokers topic to those rules, particularly regarding several types of actions like kiosks, fee processors and pockets suppliers. The absence of a proper digital asset registry complicates compliance for brokers, together with centralized exchanges and decentralized platforms.

Downside of digital asset intermediary

The broad definition of “digital asset intermediary” within the proposed rules might contain a number of brokers in a single transaction. For instance, if a consumer makes use of a self-hosted pockets with a DeFi platform for a token swap, each the pockets supplier and DeFi platform could be thought-about middlemen.

Not like securities guidelines, there isn’t any exemption for a number of middlemen, so every should file their very own Kind 1099-DA with the IRS and taxpayer. This might confuse taxpayers, resulting in over-reporting or discrepancies with IRS information, including to taxpayer burden.

Moreover, proposed rules’ wallet-by-wallet identification method might pose challenges for taxpayers holding belongings with low bases in particular wallets. They could must switch high-basis belongings to these wallets to establish them.

Crypto brokers: Who’re they?

The Infrastructure Funding and Jobs Act, efficient from Jan. 1, 2024, requires crypto brokers to report transactions over $10,000 to the IRS. This has sparked controversy attributable to perceived burdens and implementation challenges.

Brokers should submit detailed stories to the IRS inside 15 days of qualifying transactions, together with sender info. Lack of IRS steering leaves customers not sure about compliance, particularly concerning miners, validators, decentralized exchanges and nameless transactions.

Beginning Jan. 1, 2025, proposed rules would mandate brokers like digital asset buying and selling platforms, fee processors and particular hosted pockets suppliers to report gross proceeds utilizing Kind 1099-DA and furnish payee statements to prospects.

Moreover, underneath sure circumstances, brokers would wish to incorporate acquire/loss and foundation particulars for gross sales occurring after Jan. 1, 2026, on these returns and statements to help prospects in tax preparation.

Based on the PwC report, IRS anticipates receiving an unprecedented quantity of “eight billion” 1099-DA stories yearly, with related prices projected within the billions. Companies will face challenges implementing the proposed rules if the efficient dates stay unchanged.

Crypto trade response to IRS

Variant’s Jake Chervinsky known as out IRS proposed rules as guidelines that “do not make sense.”

He believes the IRS’s method is pushed by a notion of tax evasion, main them to depend on monetary surveillance. Chervinsky argues that the IRS overlooks expertise enabling peer-to-peer transactions with out intermediaries able to conducting KYC checks and reporting transactions.

Dangerous information: regardless of years of trade engagement with IRS explaining why “unhosted wallets” can’t be brokers, the message someway hasn’t landed.

Excellent news: guidelines that make actually no sense in any respect hardly ever survive scrutiny within the courts.

Nice information: we actually like submitting lawsuits.

— Jake Chervinsky (@jchervinsky) April 21, 2024

Jason Schwartz, tax accomplice and digital belongings co-head at Fried Frank, famous how the novel definition of digital belongings intermediary doesn’t assist to distinguish brokers.

18/ INITIAL REACTIONS. The proposed regs’ definition of digital belongings intermediary would flip web site builders into brokers if the web sites “facilitate” digital asset gross sales.

That’s unhealthy legislation and unhealthy coverage.

— CryptoTaxGuy.ETH 🦇🔊🛡️ (@CryptoTaxGuyETH) August 27, 2023

On Nov. 7, 2023, the DeFi Schooling Fund (DEF) filed a short supporting James Harper’s enchantment towards the IRS, aiming to restrict the federal government’s entry to consumer transaction historical past on cryptocurrency platforms.

Harper was one in every of 1000’s of Coinbase customers whose information was disclosed to the IRS in 2017, prompting a authorized problem for stronger digital privateness rights. DEF argues that rules proposed on Aug. 27 would develop the definition of “dealer” too broadly, impose burdens on people and entities unable to conform, whereas jeopardizing privateness.

The IRS’s “dealer rule” hasn’t been finalized, but it surely seems like Treasury is actually going to take the place that “unhosted pockets suppliers” are “brokers” 🤦♂️🤦♂️

IRS launched draft 1099 type for digital asset “brokers”: https://t.co/wH2IVWZ2gX pic.twitter.com/6oVNNmwPXO

— Miller (@millercwl) April 19, 2024

IRS steering sources

The remedy of cryptocurrency is topic to restricted steering, together with:

- Discover 2023-34, providing steering on sure convertible digital currencies.

- The Infrastructure Funding and Jobs Act of 2021, which addresses digital asset info reporting for brokers.

- Proposed Laws on digital asset reporting launched Aug. 25, 2023.

- Income Ruling 2023-14, which discusses the inclusion of staking rewards in earnings for cash-method taxpayers.

- Discover 2023-27, clarifying that NFTs must be handled as collectibles.

- Income Ruling 2019-24, offering steering on exhausting forks and air drops.

- FAQ, as up to date on the IRS web site.